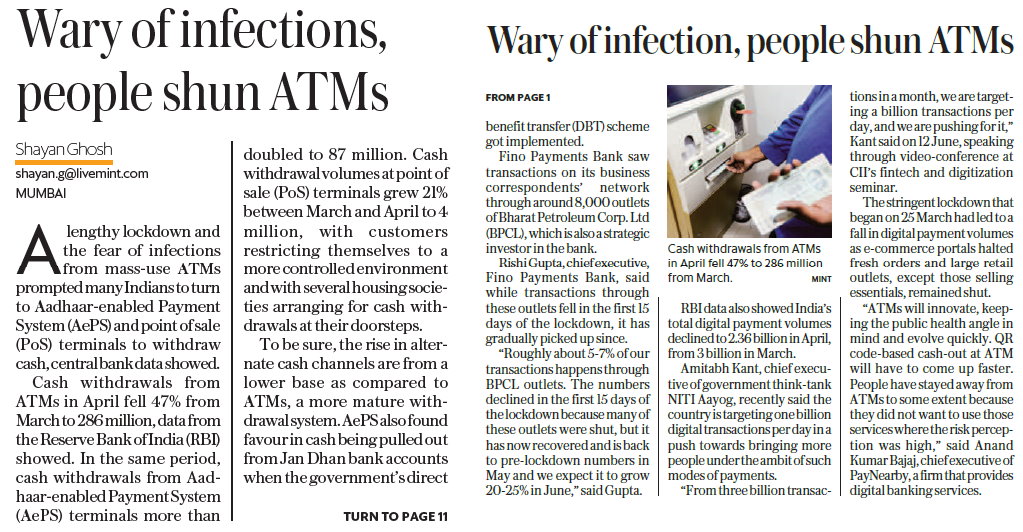

Catalyst to digitize cash for mass market customers to enable them to enjoy benefits of digital commerce

Mumbai, December 3rd: PayNearby, India’s largest hyperlocal fintech startup, has partnered with YES Bank and National Payments Corporation of India (NPCI) to launch PayNearby Shopping Card, enabling its retail partners to derive maximum benefits of digital commerce in the mass market category. The new offering aims to enable PayNearby retailers to seamlessly consume a range of digital services, like ecommerce, e-learning, online gaming, online music and videos, monthly recharges and utility payments in a secure, risk free mode.

India has a large underbanked, un-carded, digitally shy population who still transact in cash. Mass market penetration of digital services in India is challenged because of the limited adoption of digital money. The launch of PayNearby Shopping Card powered by RuPay is aimed to enable mass market adoption, so that cash digitization options are available at grass root levels.

The PayNearby Shopping Card will offer our retailers a safe and simple payment instrument to fulfil their digital commerce requirements. The card is easy to use and is enabled across 10 lakh plus PayNearby retail touch points, across 17,000 plus PIN codes in the country. The retailers can avail the card by completing the KYC. The maximum wallet balance at any point in time can be Rs. 1 Lakh and users can transact upto Rs. 5 lakh monthly and Rs. 25 lakhs annually.

PayNearby is committed to uplifting the technology shy population and taking them up the digital curve so that benefits of digital advancements can be more widespread. Active usage of these cards will be promoted through tailored campaign for both retailers and consumers. The new offering aims to boost online transactions across platform in ecommerce purchase, monthly utility payments, mobile recharges, online education subscriptions and more. In post COVID era, when contactless payments and digital commerce have become so significant to avail services, PayNearby aims to enable masses to access these benefits through PayNearby Shopping Card powered by RuPay.

The prepaid card is a secured payment instrument and mitigates the risk of cyber fraud, especially in case of high-volume transactions. While it operates very similar to a debit card, unlike the latter, the PayNearby Shopping Card is linked to a PayNearby wallet rather than a bank account. Users can load as much or as little money as they are comfortable with, thus minimizing risks while securing payments. Fraud protection mechanisms put in place ensure transactions are secure and there is no data compromise.

One of the most salient features of the offering is that it enables the user to seamlessly lock/unlock the card digitally while also offering a summary of the transaction statement which in turn helps users to keep their spending under check.

Commenting on the announcement, Anand Kumar Bajaj, Founder, MD & CEO, PayNearby stated, “We are delighted to partner with NPCI to launch the PayNearby Shopping Card powered by RuPay, a virtual prepaid instrument that ensures secure transactions. Our Digital Pradhan network has been at the forefront of the pandemic, serving as corona warriors and providing seamless banking at the grassroots level. We have been processing over Rs. 100 crore transactions daily since the lockdown, and handling large volumes.

The launch of PayNearby Shopping Card powered by RuPay will act as a catalyst in our cash digitization efforts and help us uplift local communities by enabling access to a lot of digital services, which were earlier limited to 10% of India’s population who had access to digital money. It is our duty to ensure that our retailers and our customers get the maximum benefit of digital advancements in these challenging times, while assuaging any concerns of misuse and cyber frauds.

PayNearby retailers offer a host of non-financial services such as travel ticket booking, utility bill payment and mobile recharges among others to the local population which requires digital mode of payments. Additionally, where cash on delivery (COD) is not available it becomes a challenge for a customer to avail ecommerce and other services as they are required to pay digitally in advance. These customers are unbanked and underbanked and do not have access to digital payment instruments. The virtual prepaid card can play the role of an enabler offering access to assisted agent banking as the retailer can seamlessly pay for the customer using the PayNearby Shopping Card.”

Praveena Rai, COO, NPCI said, “We are pleased to partner with PayNearby and launch the PayNearby Shopping Card. Through this strategic partnership, we endeavor to deepen the financial inclusivity in the country and empower the underbanked population with seamless digital payments facility for their day to day transactions. This initiative enables small scale local retailers to upgrade and add value to their businesses with digital commerce facility, this will also act as a driving force for local retailers to onboard into the digital payment ecosystem. We believe this collaboration is a step ahead towards realizing our vision of digital payments for all.”

About PayNearby:

Incepted in April 2016, Nearby Technologies is a fintech company offering financial/non-financial services to the underbanked and unbanked segment. Nearby Technologies works on a B2B2C model through its various brands – PayNearby, Insure Nearby, BuyNearby and few more. PayNearby empowers retailers at the first mile to offer digital services to local communities, thereby boosting financial inclusion in India. Retailer services are focused on Aadhaar based banking services, Domestic Remittances, Bill Payments, Card Payments, and insurance services among others.

It was founded by Anand Kumar Bajaj, Subhash Kumar, Yashwant Lodha & Rajesh Jha who bring with them rich experience in the field of banking, payments and other financial sectors. PayNearby is a DIPP-certified FinTech startup, partnering with various financial institutions including YES Bank, RBL Bank, ICICI Bank, State Bank of India, Axis Bank, CC Avenue, Bill Desk, NPCI, FASTag, NBFC and FMCG companies. It is the sole technology provider using Aadhaar Enabled Payment Services (AEPS) and IMPS to YES Bank, making them one of the only two fintech companies hosted by the National Payments Corporation of India (NCPI).

For more information, visit: http://paynearby.pivotroots.com/

About RuPay:

RuPay, first-of-its-kind India’s indigenous Debit and Credit payment network, was launched by National Payments Corporation of India (NPCI). It has been designed to address the evolving needs of Indian consumers, merchants and banks.

About NPCI:

National Payments Corporation of India (NPCI) was incorporated in 2008 as an umbrella organization for operating retail payments and settlement systems in India. NPCI has created a robust payment and settlement infrastructure in the country. It has changed the way payments are made in India through a bouquet of retail payment products such as RuPay card, Immediate Payment Service (IMPS), Unified Payments Interface (UPI), Bharat Interface for Money (BHIM), BHIM Aadhaar, National Electronic Toll Collection (NETC Fastag) and Bharat BillPay. NPCI also launched UPI 2.0 to offer a more secure and comprehensive services to consumers and merchants.

NPCI is focused on bringing innovations in the retail payment systems through use of technology and is relentlessly working to transform India into a digital economy. It is facilitating secure payments solutions with nationwide accessibility at minimal cost in furtherance of India’s aspiration to be a fully digital society.

For more information, visit: https://www.npci.org.in/