Mahatma Gandhi’s concept of Gramodaya, Antodaya, and Sarvodaya captures the true essence of all economic progress and development. These terms can be roughly translated as the upliftment of rural India, of the last mile, and the upliftment of all. Today, this holds particularly true than ever because for India to shine bright, rural India has to progress. It is increasingly getting clear that ‘inclusive growth’ is mandatory for smoothening our country’s journey towards economic progress. India, home to one of the most fragmented banking systems, has been rolling out new-age financial startups to widen reach, thereby pushing the agenda of financial inclusion. However, in a vastly geo-distributed population like ours, financial inclusion has been a huge challenge owing to factors such as – socio-economic influences, inhibition to adopting technology, high distribution and operational costs, and lack of inclusive growth among others.

Most of India’s population lives in villages, it is imperative that there is a robust network in place – both digital and assisted – to allow the beneficiaries to avail them. People living in rural areas are especially in dire need of financial services for a range of products – like the ease of access to savings, credit, education, working capital for entrepreneurship, and protective reasons like health insurance. Several constraints like the high cost of financial infrastructure in these areas, lack of financial literacy, and high transaction costs also discourage people from depositing savings, thereby depriving households of an opportunity to build financial assets. The key is to enable banking to be location agnostic, ensuring that irrespective of wherever people are, they have access to financial facilities.

Fintechs are driving the inclusion wagon with their tech-led solutions. They are rapidly becoming the face of financial inclusion possibilities, especially in an economically diverse and developing country like ours. The fintech industry’s growth story in India – due to its abilities and agility – indicates an enormous financial services market opportunity that has been untapped. The technological innovations aimed at breaking the barriers of the urban-rural divide are able to bring more tech-shy people within the realm of financial inclusion. With an increasing number of startups, maturing ecosystem, and favourable government stance, it is needless to say that fintech is here to stay and grow further. The idea is to nudge the fintech industry towards a path where it should make a difference – beyond an easily accessible market of the tech-savvy urban customer base.

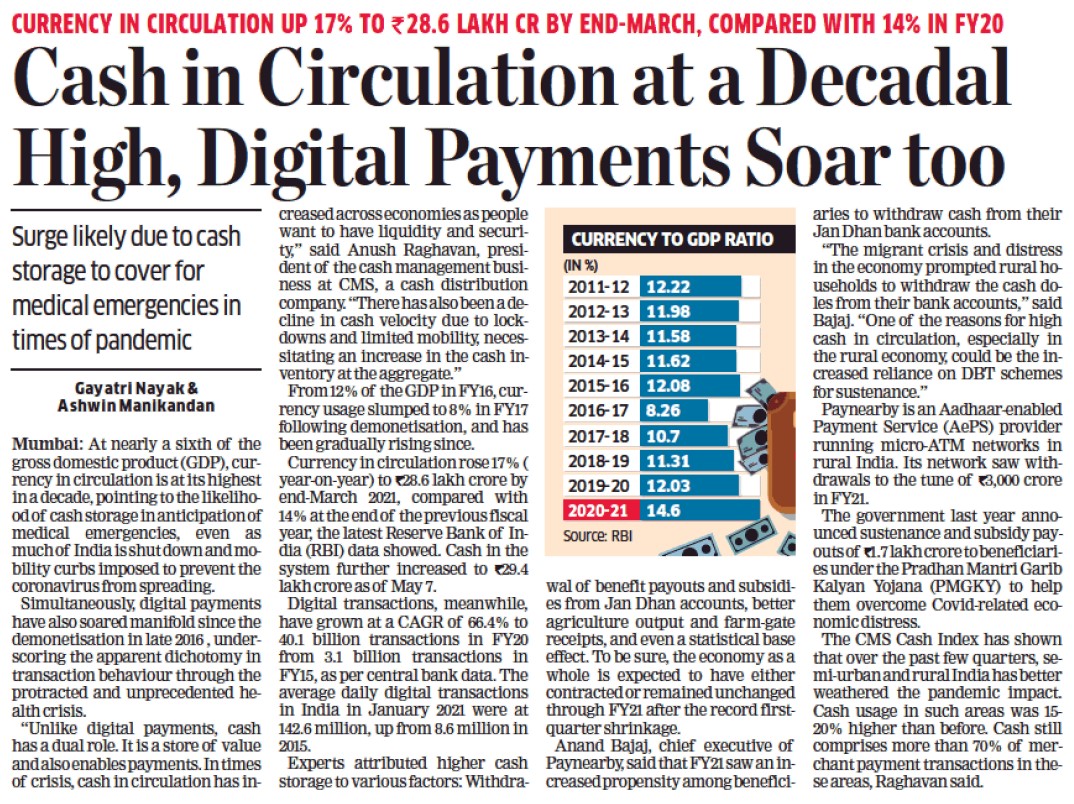

The hurdle of accessibility in underserved regions is largely being addressed by branchless banking – through business correspondents (BCs), POS terminals, and mobile banking. Their usage has only intensified since the pandemic – with more people adopting channels like Aadhaar Enabled Payment System (AePS) or micro ATMs to withdraw cash and access DBT (Direct Benefit Transfer) funds in the peak months of the lockdown when movement was heavily restricted.

To generate appeal among the rural stratum, both governments and providers need to track adoption patterns closely and understand customer needs to bring them into the ambit of financial inclusion. One main barrier to their access to formal banking channels is their irregular income flow which inhibits them from getting bank loans, saving to reap interest benefits, and even buying insurance policies, which usually have high premiums. Sachetisation of services is a way to reach the bottom of the pyramid – by customising financial offerings to be affordable to meet their future goals. It will allow communities lying outside the financial fold to save, borrow and invest securely. It will save them for future contingencies and unscrupulous moneylending channels, which often drive them further into the debt trap.

Financial products catering to the last-mile access must be of small ticket size with short tenure, aiming to meet the specific population’s needs. Sachetisation is not a novel concept – it has earlier transformed the FMCG sector (think shampoo sachets) – helping services transition from luxury to affordability. Through these ‘micro’ sizes, a systemic change can be brought about in their mindsets towards insurance, investments, and even lending. With the help of API and plug-and-play platforms, they can serve a considerable segment of the population through customised low-value, high-volume transactions. Consider the case of telecom; smaller value packs of recharge are in demand than higher value recharges.

Accessibility, usability, user-friendly, interoperability, quick decision-making, and rapid processing are key factors for offering financial services in a sachet. It would also require a change in the approach in the mind-sets of providers from a push-based offering to pull-based. The process will lead to fulfilling specific, context-based needs by altering the core product offerings.

This cohort, though often underbanked and unbanked but highly aspirational, is getting exposure to trends through internet connectivity and smartphones. At a time when big companies have notoriously been struck by a string of defaults, who are usually the recipient of large bank loans, rural regions are emerging as the saviours of the economic flux by driving consumption and it is on the banking ecosystem to ensure that it has a multiplier effect. In the end, it is only through Gramodaya and Antyodaya, we can bring an era of Sarvodaya. And, sachetisation is the way forward!

- Source – The Financial Express

- Published Date – April 1, 2021